Restrictions in the global supply of sulfur and phosphates raised production costs and caused an increase in the price of dicalcium phosphate and mineral supplements throughout 2026.

Author: Rodrigo De Mundo, zootechnician and researcher at Scot Consultoria. Analyst team: Alcides Torres · Fábio Takaku · Felipe Fabbri · Gustavo Duprat · Isabela Stevanatto · Juliana Pila · Lorenzo Cracco · Marcelo Roschel · Mariana Hauschild · Pedro Gonçalves · Roselena Sestari · Rodrigo de Mundo · Stéfany Souza. Responsible journalist: Talita Aparecida Peixoto Dias – MTB 0022766/MG.

Scot Consultoria is not responsible for business decisions made based on information contained in this report. All rights reserved. This report was prepared for the use of its subscribers and collaborators. Reproduction requires written authorization from Scot Consultoria.

The strategic input

Dicalcium phosphate (DCP) is the main source of phosphorus used in animal nutrition and a strategic input for Brazilian cattle farming. It is used in the formulation of mineral supplements and feed for cattle, poultry, swine, and fish, ensuring the supply of phosphorus and calcium, which are essential for productive and reproductive performance.

Industrially, dicalcium phosphate is produced from the reaction between phosphoric acid and a calcium source. Phosphoric acid uses phosphate rock as a raw material, a mineral resource whose supply is concentrated in a few countries, making the market dependent on the global availability of this ore.

Although Brazil possesses phosphate rock reserves and production, domestic supply does not fully meet the demand of the animal nutrition and fertilizer chain, keeping the country dependent on imports. Thus, factors such as international supply, production costs, logistics, and exchange rates influence prices in the Brazilian market.

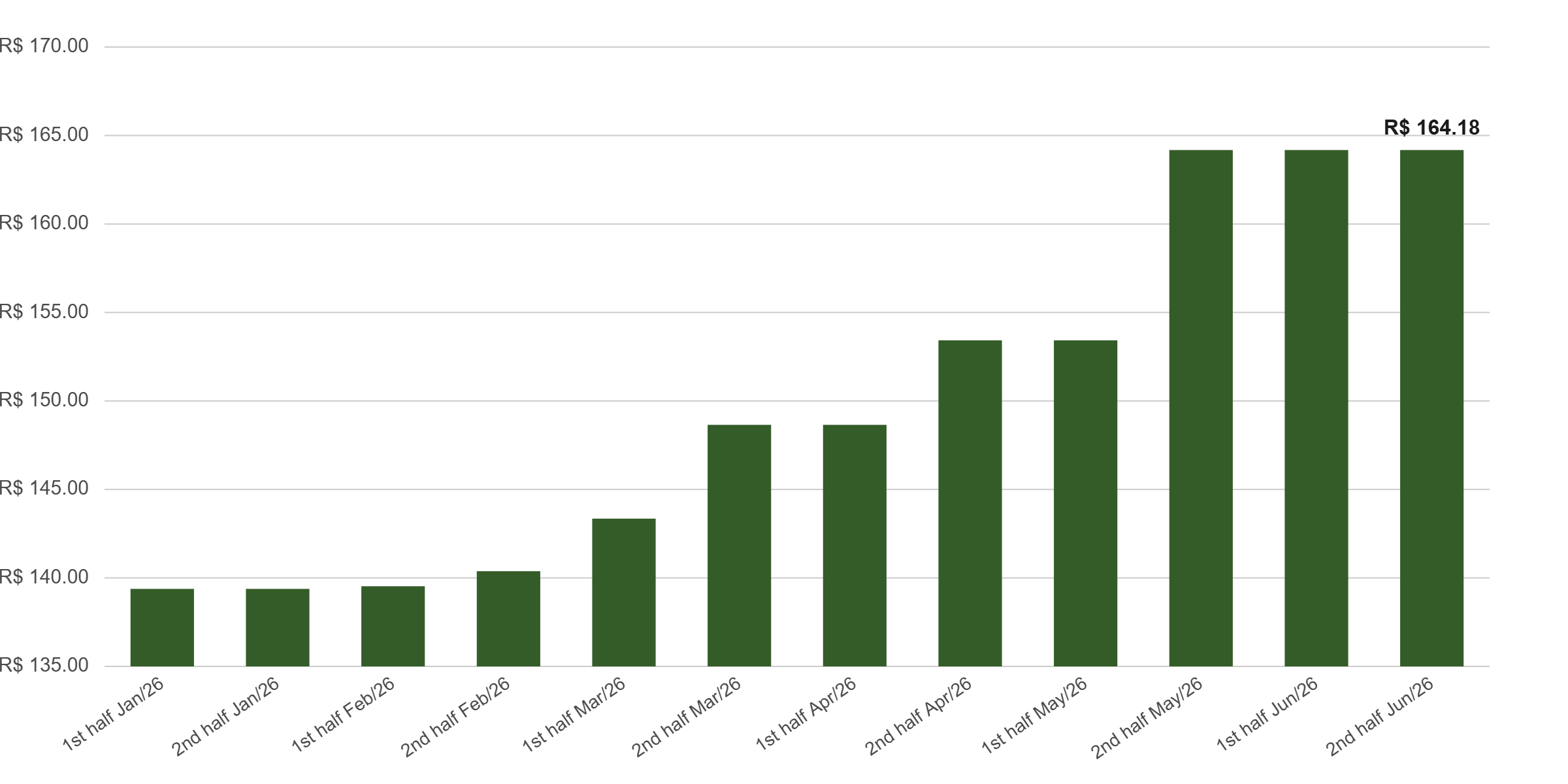

Between January and June of this year, the price rose 17.8%, averaging R$164.18 per 25 kg bag.

Evolution of the price of a 25 kg bag of dicalcium phosphate, FOB São Paulo

The impact of sulfur

The market is being marked by rising production costs, reflecting the increase in the cost of the main raw materials of the phosphate chain.

The main pressure factor came from sulfur, which is used in the production of sulfuric acid, an essential input for manufacturing phosphoric acid, the base of dicalcium phosphate. The escalation of sulfur prices raised costs for the phosphate industry.

Sulfur started 2026 under pressure, continuing the upward trend registered in 2025, when the imbalance between supply and demand supported prices (read more in edition 242 of Carta Insumos).

The global supply of sulfur has low elasticity. The product is not generated specifically for agriculture or livestock, being mostly obtained as a byproduct of petroleum refining and natural gas processing.

In 2025, this imbalance was caused by restrictions in major producing and exporting regions, such as Russia, which, in addition to decreasing production and exports, had to import the input to meet domestic demand. Furthermore, there were shutdowns and reduced performance in refining units, reducing international availability.

At the same time, demand remained firm, sustaining the consumption of sulfuric acid and, consequently, sulfur.

The conflict between the United States and Iran intensified the increase by affecting producing regions and the main logistical hub of the global sulfur trade, the Strait of Hormuz, through which about 50% of the world's supply of the product passes.

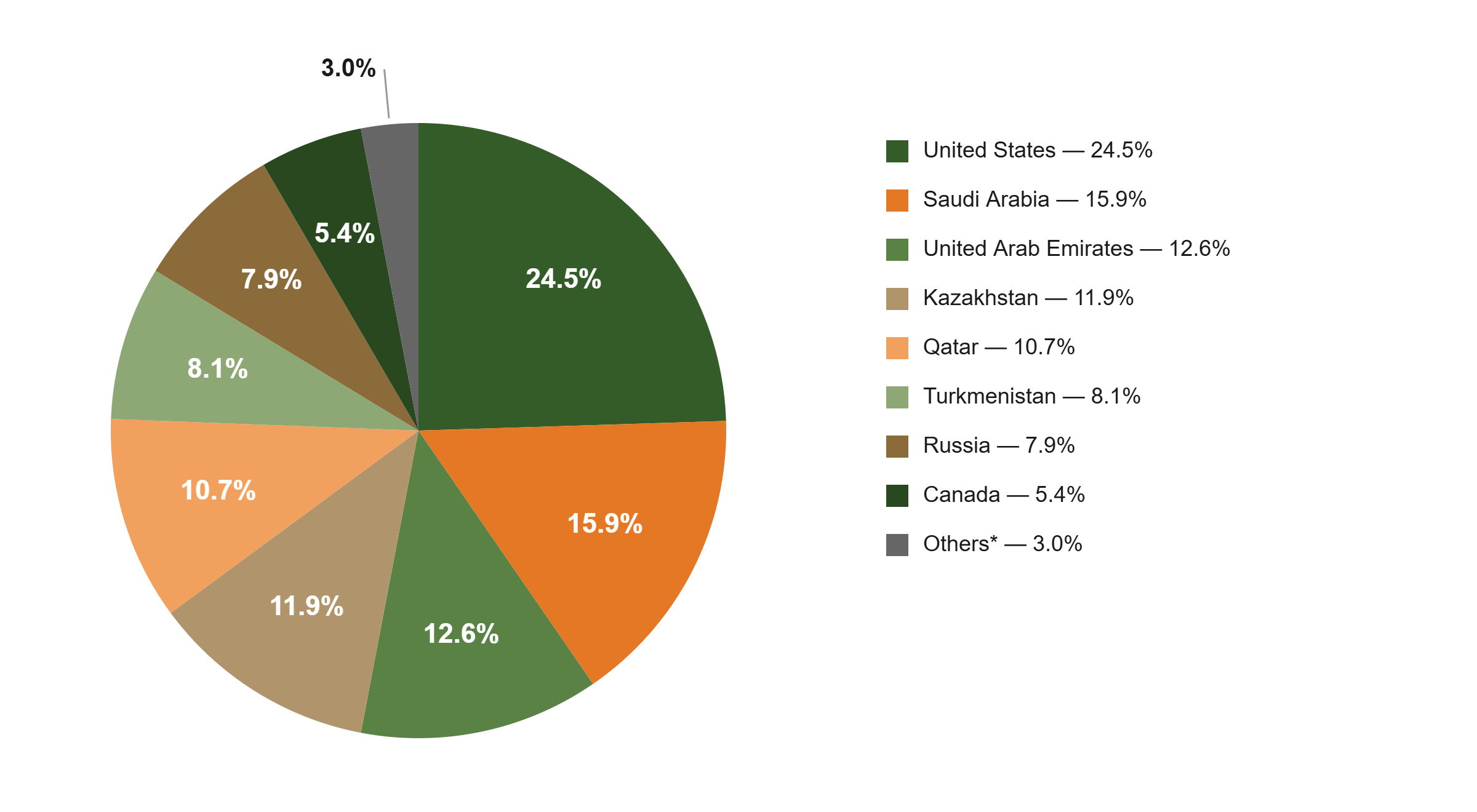

Approximately 42% of the sulfur imported by Brazil in 2025 came from the Middle East (Figure 2).

Country share in sulfur imports by Brazil in 2025 (%)

Source: Secex / Prepared by Scot Consultoria

Prices on the rise

With the closure of the Strait, the rise in freight rates, maritime insurance, and uncertainties regarding shipments, the market came under pressure. Even without production disruptions, the increased risk was enough to restrict supply, with shipments being postponed, rerouted, or negotiated with additional premiums.

In this context, the market began incorporating a risk premium, driving up prices. Additionally, there was an anticipation of purchases to secure supply.

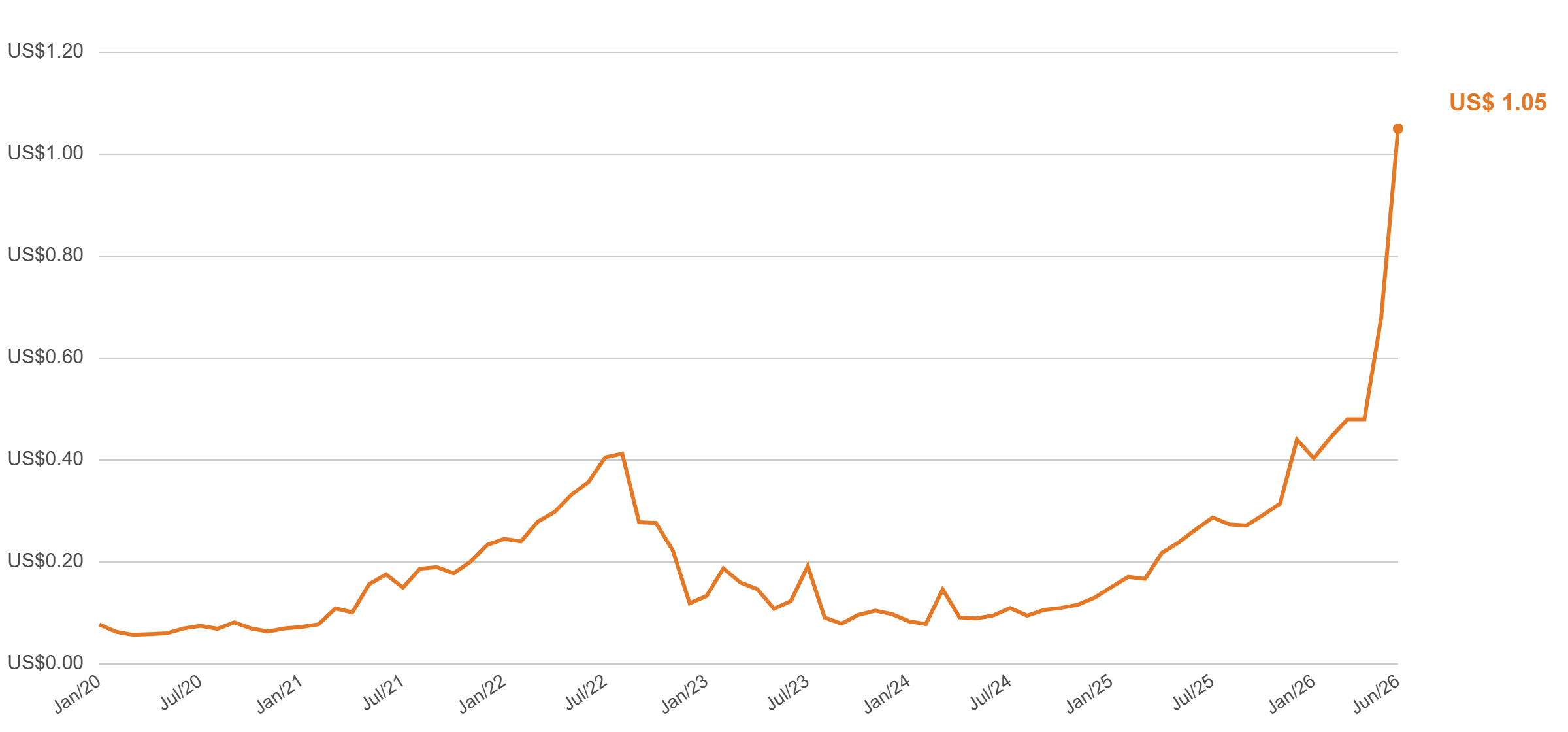

In June 2026, the price per kilogram of sulfur imported by Brazil reached its highest level in the last six years, priced at US$1.05/kg. This is an increase of 298.0% over 12 months and 595.9% compared to January 2025.

Price of sulfur imported by Brazil (US$/kg) over the last six years

In the international market, the price per ton of sulfur also reached record levels, exceeding 10.0 thousand yuan or 1.5 thousand dollars per ton, reaching 9,119 yuan or 1.3 thousand dollars on 7/14. This represents an increase of over 300% compared to the same period in 2025.

The price is presented in yuan per ton because it follows the Chinese market, one of the main global references for sulfur, since there is no single international price for the product.

Industrial sulfur price in China (CNY/ton), last five years

Global phosphate supply

The global supply of phosphates (fertilizers; phosphoric acid; some phosphate salts) remains restricted. Limitations on Chinese exports of phosphates reduced international availability, supporting prices throughout the year. As China accounts for a relevant share of world phosphate production, any restriction on its shipments affects the international market.

Since the end of 2025, China has maintained restrictions on exports of phosphate fertilizers, prioritizing domestic supply and the stability of domestic prices. In 2026, the country also restricted exports of sulfuric acid, decreasing global availability precisely at a time of sulfur scarcity.

These measures reduced international market liquidity and contributed to the price increase.

In Brazil, dependence on imports of phosphate rock, phosphoric acid, and other inputs in the chain caused the domestic market to follow this trend. Besides the increase in raw materials, maritime freight costs and exchange rates contributed to keeping dicalcium phosphate prices high during a large part of 2026.

Few substitutes, stable demand

Despite price pressure, demand remained relatively stable. Dicalcium phosphate has a low potential for substitution in animal nutrition.

Meat and bone meal (MBM) is one of the substitutes for dicalcium phosphate in the formulation of poultry and swine feed, as it provides phosphorus, calcium, and protein.

Its advantage is lower cost, in addition to adding protein to the diet. On the other hand, it presents greater variation in nutritional composition and less standardization compared to dicalcium phosphate, requiring greater care in feed formulation.

In ruminant nutrition, such as cattle, meat and bone meal cannot be used in Brazil due to sanitary restrictions related to the prevention of bovine spongiform encephalopathy (mad cow disease). Thus, for cattle farming, dicalcium phosphate remains the main source of phosphorus.

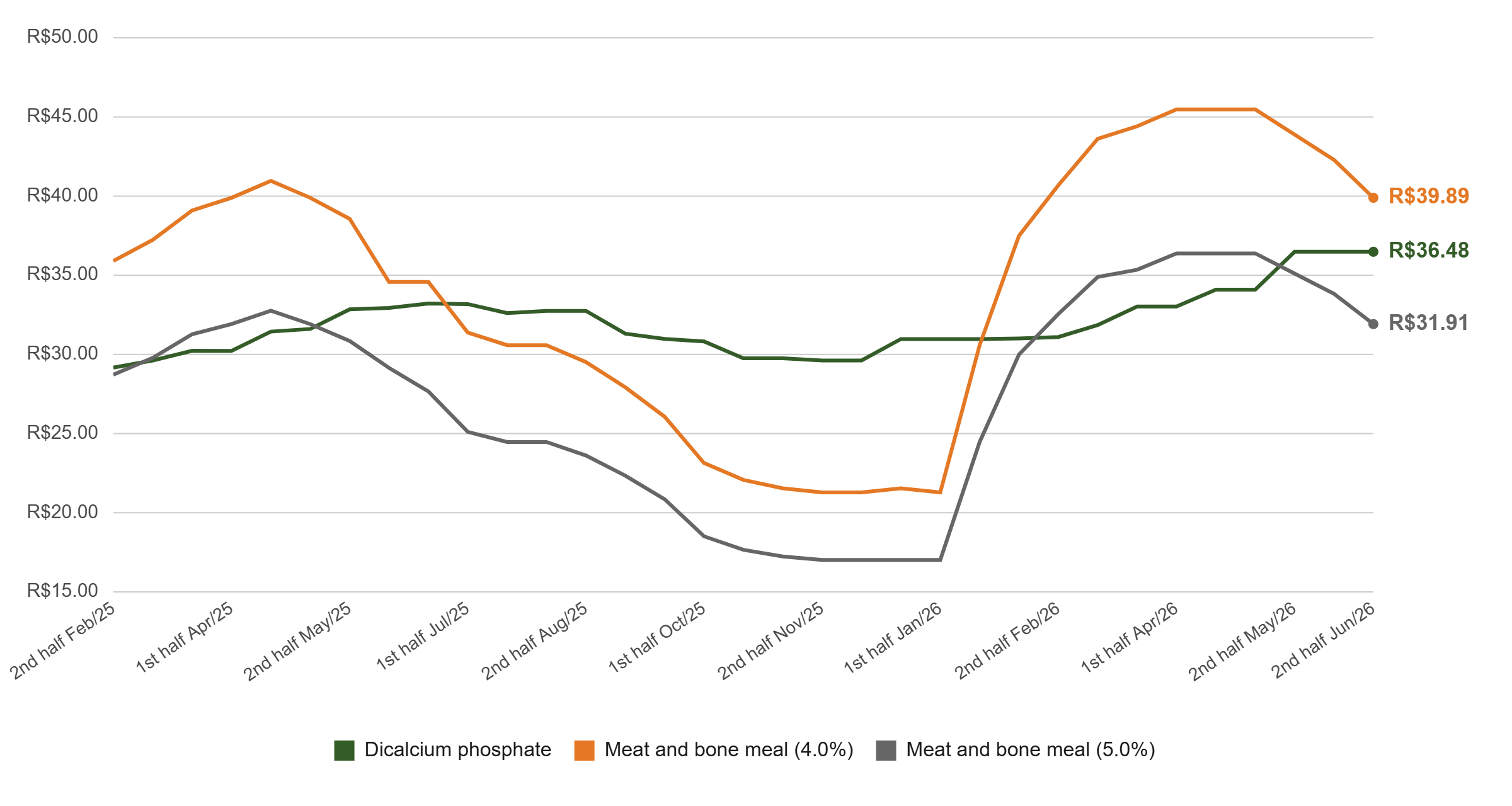

Price in R$/kg of available phosphorus: dicalcium phosphate vs. meat and bone meal

In June, the price per kilogram of phosphorus was R$36.48 for dicalcium phosphate, considering 18.0% phosphorus, and R$39.89 and R$31.91 for meat and bone meal with 4.0% and 5.0% phosphorus, respectively.

Mineral supplements on the rise

The mineral supplements market followed the upward trend in dicalcium phosphate prices. The increase was passed on to phosphorus-containing products, while the lower availability of the raw material caused sporadic supply difficulties and extended delivery times in some regions.

Between January and June of this year, mineral supplements for phosphorus supply saw an increase in their prices of close to 10.0% or more.

Evolution of the price of a 30 kg bag of mineral supplements with different phosphorus concentrations

Outlook

In the short term, the expectation is for stability to a rise in the price of dicalcium phosphate. Limited traffic in the Strait of Hormuz hinders supplies from Brazilian suppliers.

In China, sulfur stock at ports in June was estimated at 820 thousand tons, a volume 26.13% lower compared to May. Compared to the same period last year, the decline reaches 63.0%. This limits the possibility of the Asian country supplying Brazil, given that consumption is higher than replenishment at ports.